The Definitive Guide to Trump Accounts

Philosophy, Simplicity, and How They Stack Up Against the Alternatives

The Definitive Guide to Trump Accounts

Philosophy, Simplicity, and How They Stack Up Against the Alternatives

By Jim Reynolds | www.reynolds.com

July 17, 2026

A Note to Readers

This is a different kind of essay from what I normally write.

I usually write about politics, culture, history, and the events shaping the country around us. This one is more practical—and may prove far more consequential.

Trump Accounts are a new financial tool with the potential to affect the lives of millions of American children. Properly understood and wisely used, they could significantly change the long-term financial future of your children, grandchildren, and other people you love.

With considerable help from Bob 🅱️, I have done my best to untangle exactly how these accounts work, why they were designed this way, and where they fit alongside 529 plans, Roth IRAs, custodial accounts, and other familiar savings vehicles.

This is Part One. It explains the structure, philosophy, rules, advantages, and limitations of Trump Accounts.

Part Two will move from theory to real life. We will examine a wide range of family scenarios, calculate expected long-term outcomes, and compare what may happen when families contribute different amounts—or nothing at all beyond the original federal deposit.

This subject deserves more than a passing summary. The decisions families make during the next few years could echo across the lifetime of a child.

This may be the most important essay I have ever written. It could change lives.

Most Children Begin With Nothing

Most American children reach adulthood owning almost nothing.

No stocks. No retirement account. No direct stake in the companies whose growth will shape their economic future. Even in financially responsible families, money saved for a child is usually aimed at a specific expense—college, a car, or perhaps the first months away from home.

At 18, this described me. I had no investments and no meaningful understanding of compounding. Like most young people of my generation, I entered adulthood prepared to work—but not yet prepared to own.

Trump Accounts begin with a different idea.

Every American child should have an opportunity to own a real piece of the American economy from the earliest possible age. That ownership should begin before the child can work, continue across the longest possible period of compounding, and require as few financial decisions as possible.

This is not merely another savings account.

It is an ownership account.

That distinction explains nearly everything about its design.

Trump Accounts are not intended to finance one predetermined expense. They do not require parents to become amateur portfolio managers. They do not encourage stock-picking, frequent trading, complicated tax strategies, or expensive financial advice.

The basic formula is deliberately plain:

Start early. Own a broad cross-section of American business. Keep costs extremely low. Leave the money alone.

That is the philosophy.

Bob 🅱️ says: “Finally, a government program built around the revolutionary idea that people should stop fiddling with things.”

What Is a Trump Account?

A Trump Account—formally established under Section 530A of the tax code—is a new type of individual retirement account created for an eligible child.

The child is the account owner and beneficiary. While the child is young, a parent, guardian, or other authorized adult serves as the responsible party and manages the account on the child’s behalf.

An account can generally be established for a child who has not reached age 18 by the end of the year in which the election is made. Unlike a conventional Roth or traditional IRA, the child does not need earned income for contributions to be made during the special childhood growth period.

The central provisions are straightforward:

Eligible children born from January 1, 2025, through December 31, 2028, can receive a one-time $1,000 federal contribution if the required election is made.

Parents, relatives, employers, charities, governmental entities, and others may also contribute under the applicable rules.

Ordinary family and employer contributions are generally subject to a combined annual limit of $5,000, indexed for inflation after 2027.

Certain government and charitable contributions may be treated separately from that ordinary limit.

The money grows without annual taxation inside the account.

During the childhood growth period, distributions are generally prohibited.

Investments are restricted to qualifying low-cost funds tracking broad American stock indexes.

Most of the special childhood restrictions end before January 1 of the calendar year in which the beneficiary turns 18. Traditional IRA rules then generally begin to apply.

The federal contribution is important, but it should not obscure the larger innovation. The account creates a structure through which families, employers, philanthropists, and governments can all help a child accumulate productive assets.

The government provides the opening stake.

The architecture permits others to build upon it.

The Investment Restriction Is the Feature

The most unusual provision may also be the most intelligent.

During the protected growth years, Trump Account money cannot be scattered among speculative stocks, leveraged investments, fashionable trading strategies, or high-fee financial products. It must be invested in qualifying low-cost mutual funds or exchange-traded funds that track broad indexes of American companies.

At launch, contributions are directed into the State Street SPDR Portfolio S&P 500 ETF. Treasury has also selected additional low-cost choices—expected to become available in the coming months—tracking the S&P 500, the total American stock market, and the broader S&P 1500.

Some people may see those limitations as paternalistic.

I see them as the central strength of the program.

The restrictions eliminate several of the most common ways ordinary investors damage their own results:

Paying unnecessarily high fees.

Trading too frequently.

Chasing whatever performed best last year.

Concentrating money in a few exciting companies.

Selling during market declines.

Allowing an adviser to turn a simple account into a complicated financial product.

A child does not need a clever portfolio.

A child needs time.

The account is therefore designed around the assumption that most people will do better owning the market than trying to beat it. It replaces hundreds of possible financial decisions with one durable rule: buy a broad basket of productive American companies and hold it.

The restriction is not a bug.

It is the feature.

Bob 🅱️ says: “You know what ruins a perfectly good investment plan? Investors.”

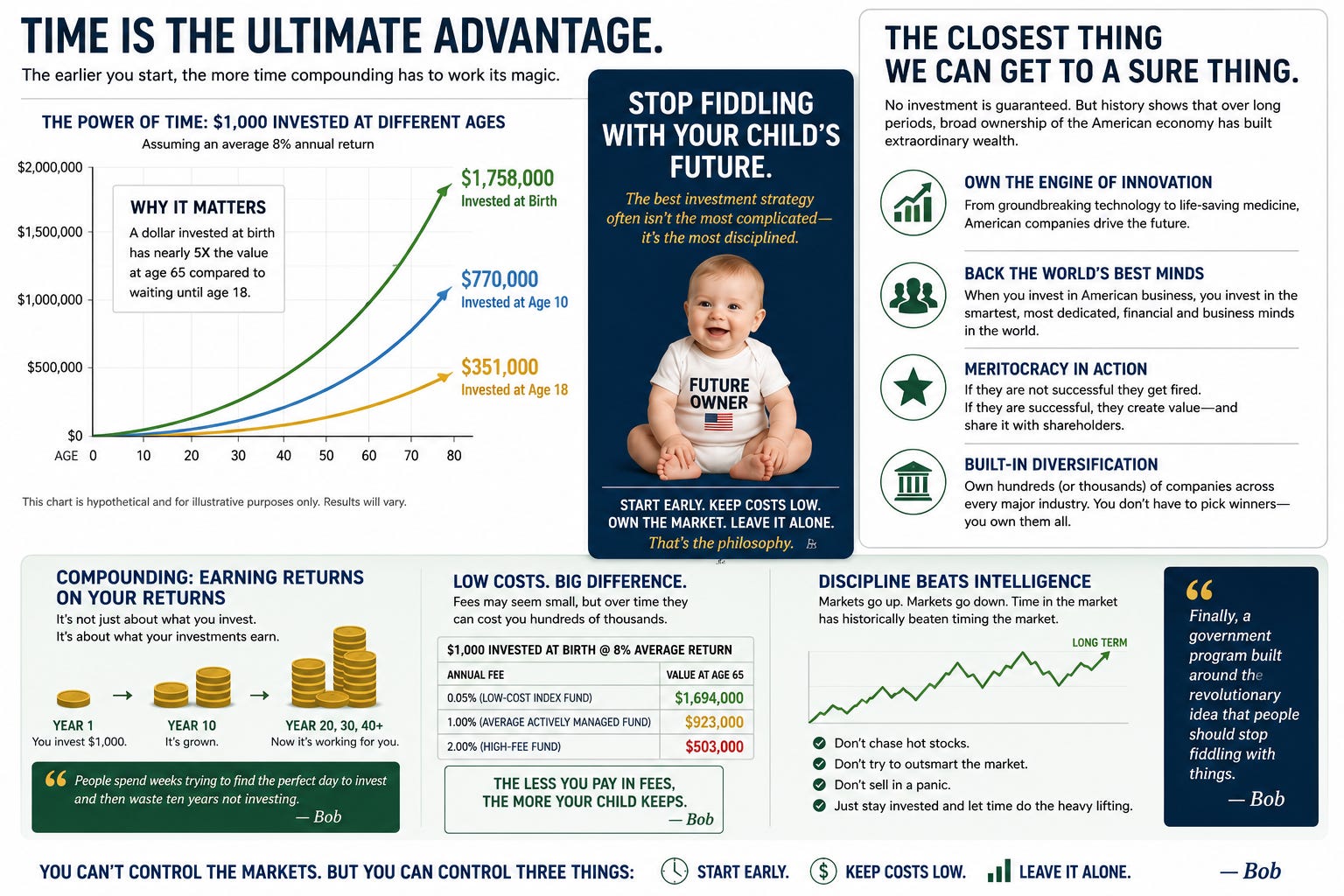

Why Starting at Birth Changes the Mathematics

Time is the most powerful variable in long-term investing because compounding does not proceed in a straight line.

Investment returns begin earning returns of their own. Given enough time, the growth generated by the account can eventually become much larger than the original deposits.

A dollar invested at birth receives approximately twice the compounding runway of a dollar invested at age 10. It receives nearly three times the runway of a dollar first invested at age 18.

That does not guarantee a particular outcome.

Stocks decline. Markets can remain weak for years. No honest discussion of equity investing should pretend otherwise.

But a newborn child has something most adult investors can never recover:

An extraordinarily long investment horizon.

Over many decades, a broad index of large American businesses has historically produced substantial growth despite recessions, wars, inflation, political crises, technological upheaval, and repeated market crashes. The path has never been smooth, but the productive capacity of the American economy has proved remarkably durable.

Trump Accounts are built to exploit that long horizon.

The child does not need to predict the next recession. The parents do not need to identify the next great company. Nobody needs to determine whether this week is the perfect time to invest.

The account simply begins.

Bob 🅱️ says: “People spend weeks trying to find the perfect day to invest and then waste ten years not investing.”

Why Costs Matter More Than They Appear

An annual fee of one-half or one percent may not sound consequential. Over several decades, however, the investor loses not only the fee but also every future dollar that the deducted money might have earned.

That loss compounds too.

The qualifying investment funds are therefore subject to stringent cost limitations. Treasury’s initial lineup consists of index funds with expenses well below the statutory ceiling.

This leaves nearly all of the market’s return inside the child’s account.

The structure also leaves little room for anyone to sell elaborate management services, constantly rearrange the portfolio, or collect substantial fees for making decisions that the account was specifically designed to avoid.

There is very little to manage.

That is intentional.

Bob 🅱️ says: “If your financial adviser needs twelve charts to explain why he deserves one percent a year, hide your wallet.”

The Tax Treatment

Trump Accounts are commonly described as custodial traditional IRAs, but their tax treatment has several distinct features.

The account grows tax-deferred. Dividends and investment gains are not taxed annually while they remain inside the account.

Contributions made by individuals are generally after-tax contributions. Those deposits create basis in the account. Federal seed money, employer contributions, certain other deposits, and investment earnings may represent taxable funds.

That does not mean a beneficiary can necessarily withdraw all family contributions first and declare them tax-free. As with other traditional IRA arrangements containing both taxable and after-tax money, distributions generally include a proportionate allocation between taxable funds and nontaxable return of basis.

The distinction matters.

A Trump Account is not a Roth IRA. Its chief tax advantage during childhood is tax deferral, not a blanket promise that all future withdrawals will be tax-free.

Its largest advantage may not be tax treatment at all.

It may be the combination of early entry, outside contributions, low costs, broad diversification, and enforced patience.

What Happens at 18?

The account does not simply vanish on the child’s eighteenth birthday.

The special childhood growth period generally ends before January 1 of the year in which the beneficiary turns 18. After that point, most of the special Trump Account restrictions cease and the ordinary rules governing traditional IRAs generally begin to apply.

Depending on the account arrangement, the balance may remain in the Trump Account or be transferred trustee-to-trustee into a conventional traditional IRA.

This transition gives the young adult more control—but also introduces more temptation.

The owner may eventually have access to withdrawal provisions available under IRA law, including certain exceptions for education, a first home, disability, or other permitted circumstances. Taxes and possible penalties will depend on the nature of the money and the reason for the distribution.

But legal access should not be confused with financial wisdom.

The greatest value may come from doing nothing.

An account that has already been compounding for nearly two decades can become extraordinarily powerful if allowed to continue for another thirty or forty years. A young adult who regards the money as retirement capital rather than spending money may have been handed something far more valuable than the original balance suggests.

The account begins as a gift from adults.

Its ultimate success will depend on the judgment of the adult the child becomes.

Bob 🅱️ says: “The account survives childhood. Whether it survives the first sports car is another question.”

How Trump Accounts Compare With Taxable Custodial Accounts

A conventional UGMA or UTMA custodial brokerage account offers far greater flexibility.

The money can generally be invested in a wide variety of assets and later spent for virtually any purpose benefiting the child. Contributions are not governed by the Trump Account’s $5,000 annual ceiling, although ordinary gift-tax rules still apply.

That flexibility has real value.

Taxable brokerage accounts also receive capital-gains treatment on qualifying investment gains rather than having all taxable distributions treated under traditional IRA rules. Carefully managed long-term holdings may therefore receive more favorable tax treatment.

But taxable accounts have disadvantages:

Dividends and realized gains can generate annual taxes.

Kiddie-tax rules may apply.

The custodian can overtrade or speculate.

High-fee investments remain available.

The child generally receives control at the age dictated by state law, often 18 or 21.

Nothing prevents the account from being spent immediately once control passes.

A disciplined family can build an excellent custodial brokerage account by using one low-cost index fund and rarely touching it.

The difficulty is that discipline is optional.

Trump Accounts place much of that discipline inside the structure itself.

The taxable account wins on flexibility. The Trump Account wins on simplicity, tax deferral during the growth years, access to possible outside contributions, and protection against many common investment mistakes.

How Trump Accounts Compare With 529 Plans

A 529 plan is designed primarily for education.

Contributions grow tax-deferred, and withdrawals used for qualified educational expenses are generally tax-free. Depending on the state, contributors may also receive a state income-tax deduction or credit.

Contribution limits are usually far higher than those of Trump Accounts. The parent or other account owner normally retains control and can change beneficiaries when permitted.

For families confident that substantial education expenses lie ahead, the 529 remains an extraordinarily strong vehicle.

But its strength is also its limitation.

The account is tied principally to education. Rules have become more flexible over time, and limited transfers to Roth IRAs may be possible under certain conditions, but a 529 is still fundamentally an education account.

A Trump Account serves a different purpose.

It is meant to establish long-term ownership. The money is not mentally earmarked for tuition at age 18. It can remain invested across the beneficiary’s entire adult life.

The accounts should therefore not be treated as natural enemies.

A family expecting significant college costs may put most of its own education savings into a 529, particularly when a state tax benefit is available. At the same time, it would usually make sense to capture any federal seed, employer contribution, or charitable money available through a Trump Account.

The 529 pays for education.

The Trump Account begins building ownership.

Many families will sensibly use both.

How Trump Accounts Compare With Custodial Roth IRAs

The Roth IRA remains one of the finest long-term investment vehicles ever created.

Contributions are made with after-tax money. Growth can eventually be withdrawn tax-free when the requirements for a qualified distribution are satisfied. Contributions themselves—not necessarily investment gains—can generally be withdrawn without tax or penalty.

But a Roth IRA has one major barrier for children:

The child must have earned income.

A toddler cannot ordinarily have a Roth IRA simply because the grandparents want to contribute. A teenager with a legitimate summer job can. Contributions are limited to the child’s eligible compensation or the annual IRA ceiling, whichever is lower.

Trump Accounts fill the years before earned income exists.

They permit the ownership process to begin at birth. When the child eventually starts working, the Roth can become an additional—and often superior—destination for new long-term contributions.

The two vehicles can therefore form a natural sequence:

Open the Trump Account during childhood. Capture the federal seed and any available family, employer, charitable, or governmental contributions. Once the child has genuine earned income, begin funding a Roth IRA as well.

The Trump Account starts the clock.

The Roth extends the strategy.

Other Alternatives

Coverdell Education Savings Accounts can provide tax advantages for educational expenses, but their annual contribution limits are low and eligibility is restricted by income rules.

Trusts can provide far greater control over when and how a beneficiary receives money. They can be useful for substantial estates, vulnerable beneficiaries, or families with complicated objectives. But trusts also bring legal expense, administrative burdens, and complexity far beyond what most families need for routine child investing.

A parent can also maintain a brokerage account in the parent’s own name and privately intend the money for the child. That preserves complete control. It also means the money legally remains the parent’s property and loses some of the psychological power of telling a child:

This is yours.

You own part of the country’s productive economy.

That sense of ownership may prove important.

The Financial-Education Effect

Most children encounter investing as an abstraction—if they encounter it at all.

They may hear that stocks rise over time. They may be told to begin saving for retirement. They may complete a classroom exercise involving imaginary money.

A Trump Account makes the lesson real.

The newly launched account platform allows families to view balances, track performance, arrange recurring contributions, and use financial-education resources.

A parent can show a child that the account owns pieces of hundreds or thousands of American businesses. The child can watch the balance rise, decline, recover, and compound.

A market downturn then becomes more than frightening television coverage. It becomes an opportunity to explain why businesses fluctuate in value and why long-term owners do not panic.

A dividend becomes more than a vocabulary word.

It becomes money generated by something the child owns.

The account can teach a foundational lesson that schools often neglect:

Wages come from work.

Wealth is built through ownership of productive assets.

Bob 🅱️ says: “Schools will teach children seventeen kinds of identity before they explain what a dividend is. Somebody had to step in.”

What Trump Accounts Do Not Solve

Trump Accounts should not be oversold.

A $1,000 federal contribution will not make every child wealthy. Families with more disposable income will still be able to contribute more than families living paycheck to paycheck. Investment returns are never guaranteed. A young adult can eventually make poor decisions with the money.

The annual ordinary contribution limit is modest. Future withdrawals may create ordinary taxable income. The account is less flexible than a taxable brokerage account and less tax-advantaged for education than a properly used 529.

Nor does the program eliminate the need for Social Security, retirement saving, education planning, emergency funds, or sound financial judgment.

It does one important thing exceptionally well:

It gives a child an early foothold in the ownership economy.

That is enough.

A public policy does not need to solve every financial problem to represent a substantial improvement.

The Larger Philosophy

For generations, public policy has focused primarily on income: wages, benefits, tax credits, subsidies, and transfer payments.

Trump Accounts introduce a different emphasis.

Assets.

Income helps people meet today’s needs.

Assets connect them to tomorrow’s growth.

A child who owns shares in a broad American index is not merely watching the economy from the outside. That child participates in the success of factories, technology companies, transportation networks, retailers, financial institutions, energy producers, pharmaceutical developers, and thousands of other enterprises.

The account makes capitalism personal.

That may eventually become more important than the original $1,000 deposit.

A society of owners thinks differently from a society divided permanently between people who own productive assets and people who do not. Ownership encourages patience. It teaches delayed gratification. It turns business growth from someone else’s good fortune into a shared benefit.

It also gives children time—the one resource that no government program can provide retroactively.

Start at birth.

Keep costs low.

Own the market.

Do not interrupt the compounding.

It is hard to imagine a simpler investment philosophy.

It is equally hard to improve upon it.

What Should Families Actually Do?

The general principles are clear, but families do not live in the abstract.

Should grandparents make one large contribution or smaller annual gifts? Should a middle-income family favor the Trump Account or the 529? What changes when an employer offers a contribution? What should happen when the child gets a first job and becomes eligible for a Roth IRA? What if the family can contribute nothing at all beyond claiming the federal seed?

Those questions deserve more than a paragraph at the end of a general guide.

They deserve their own article.

In the follow-up, we will examine a series of real-world families—from those able to contribute nothing to those considering the full annual amount—and follow the money through childhood, early adulthood, and retirement.

We will look at the child who receives only the original $1,000.

The grandparents who contribute every birthday.

The working family dividing its money between a Trump Account and a 529.

The teenager who gets a first job and becomes eligible for a Roth.

The employer contribution that quietly grows into something substantial.

And the fortunate child whose family contributes the maximum from birth.

The rules tell us how Trump Accounts work.

The scenarios will show us what they can become.

Real money. Real ownership. Decades of compounding in the productive capacity of the American economy.

That is the philosophy—and that is why the structure was built the way it was.